SuperSeed Capital Ld - Interim Results for Q2 and H1 2025

Announcement provided by

SuperSeed Capital Limited · WWW29/08/2025 07:00

SUPERSEED CAPITAL LIMITED

(the "Company")

UNAUDITED INTERIM RESULTS FOR Q2 AND THE HALF-YEAR ENDING 30 JUNE 2025

SuperSeed Capital Limited, a company established as a venture capital fund of funds for early-stage AI/SaaS companies, announces unaudited results for Q2 2025 and the six-months ending 30 June 2025. The Company invests in technology-led innovation, primarily through funds managed by SuperSeed Ventures LLP (the "Investment Manager"). The Company's principal investment to date is in SuperSeed II LP (the "Fund").

Financial Highlights for Q2 2025:

· NAV per share has held at

· A total of

Fund Portfolio and Investment Highlights:

· The Fund portfolio averaged 61% annualised revenue growth, and as at the end of Q2 TVPI had reached 1.27x, IRR was at 15.65% and DPI (Distributed to Paid in Capital) at 0.14x.

Outlook for Q3 2025:

· Two new companies were added to the Fund portfolio in early Q3 2025 (Ploy and Fit Collective).

· Continued investment activity, with the Fund expecting to make a further 2-4 new investments before the Investment Manager shifts focus from the investing phase to overseeing the development and maturing of the portfolio companies held by the Fund.

· The Fund continues to back founders who build inevitable solutions to urgent problems.

Mads Jensen, Managing Partner of the Investment Manager, commented:

"The portfolio demonstrates what patient capital achieves. While markets ignore Chinese models pricing at 1/77th and obsess over NVIDIA's next quarter, our companies quietly compound value by solving real problems for real customers. The winners won't be those with the biggest models or most hype, but those who translate AI capabilities into customer outcomes. This positions SuperSeed Capital well in the current market, and we continue to be positive on the prospects for 2025 and beyond."

For more information, please contact:

|

SuperSeed Capital Limited |

+44(0) 203 405 3060 |

|

Mads Jensen, Investment Manager |

|

|

|

|

|

VSA Capital - AQSE Corporate Adviser and Broker |

+44(0) 203 005 5000 |

|

Corporate Finance: Andrew Raca / Dylan Sadie |

|

About SuperSeed Capital Limited

SuperSeed exists to back

Forward-looking statements

This announcement contains statements that are or may be forward-looking statements. All statements other than statements of historical facts included in this announcement may be forward-looking statements, including statements that relate to the Company's future prospects, developments and strategies. The Company does not accept any responsibility for the accuracy or completeness of any information reported by the press or other media, nor the fairness or appropriateness of any forecasts, views or opinions express by the press or other media regarding the Group. The Company makes no representation as to the appropriateness, accuracy, completeness or reliability of any such information or publication.

Forward-looking statements are identified by their use of terms and phrases such as "believe", "targets", "expects", "aim", "anticipate", "projects", "would", "could", "envisage", "estimate", "intend", "may", "plan", "will" or the negative of those, variations or comparable expressions, including references to assumptions. The forward-looking statements in this announcement are based on current expectations and are subject to known and unknown risks and uncertainties that could cause actual results, performance and achievements to differ materially from any results, performance or achievements expressed or implied by such forward-looking statements. Factors that may cause actual results to differ materially from those expressed or implied by such forward looking statements include, but are not limited to, those described in the Risk Management Framework section of the Company's most recent Annual Report. These forward-looking statements are based on numerous assumptions regarding the present and future business strategies of the Group and the environment in which it is and will operate in the future. All subsequent oral or written forward-looking statements attributed to the Company or any persons acting on its behalf are expressly qualified in their entirety by the cautionary statement above. Each forward-looking statement speaks only as at the date of this announcement. Except as required by law, regulatory requirement, the Listing Rules and the Disclosure Guidance and Transparency Rules, neither the Company nor any other party intends to update or revise these forward-looking statements, whether as a result of new information, future events or otherwise.

Investment Manager's Review

AI Drives the Economy, Exactly as Predicted

Despite turbulence-tariffs pushing baseline rates to 15% on EU goods, inflation keeping the ten-year Treasury stubbornly above 4.2%, and interest payments consuming 18.4% of federal revenues, equity markets keep powering ahead. Since the April correction, the S&P 500 gained 22.9% through August 11 and the Magnificent Seven surged 44.8%.

The driver is artificial intelligence. Microsoft, Google, Amazon, and Meta alone will spend

NVIDIA exemplifies this transformation. In July, it became the first public company to reach a

The Four Labs Competing for AI Dominance

Beneath the hardware layer, four labs compete to capture value from intelligence itself: OpenAI, Anthropic, Google, and xAI.

OpenAI reached the

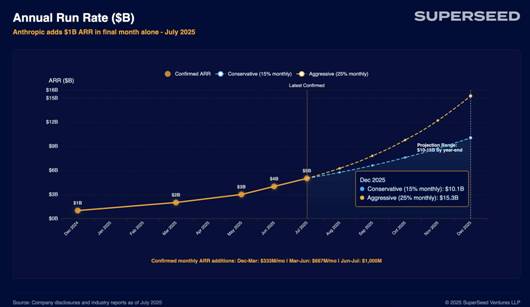

Anthropic has demonstrated the fastest growth trajectory this year. Revenue exploded from

The reason is that Anthropic's Claude models (Sonnet and Opus) dominate software development. Claude powers the tools that matter: Cursor, Windsurf, and Claude Code. Between them, these tools process 195 million lines of code weekly. While Anthropic's supremacy isn't guaranteed, it has been fabulous to watch their rise in the first half of 2025.

The battle for pole position currently plays out between OpenAI and Anthropic, with Google's Gemini and xAI's Grok competing to catch up. OpenAI maintains the scale advantage with double the revenue. Anthropic claims the momentum with 5x growth and developer mindshare. All four face the same existential question: can premium pricing survive when open-source alternatives deliver comparable performance at commodity costs?

The Threat from Chinese Open Source

While the US frontier labs have been burning billions building proprietary models, Chinese developers have gone the opposite direction. We now see great new open source models come out of

So if we assume that Chinese open source models are now nearly as good as the US models, the pricing disparity should terrify Western labs. Alibaba's Qwen3-235B costs

Using typical enterprise ratios (3:1 input to output for code review), the differential becomes stark. OpenAI's GPT-5 costs

So far, Western enterprises have been paying the premium. Some of the reasons are that the US models still hold a performance edge. Another reason is on the compliance side; enterprise support plus someone to blame when things break. Open source offers capability but less in terms of accountability. For Fortune 500 CIOs spending other people's money on critical infrastructure, that calculation still favours the expensive option.

For How Long can this Last?

Seven months ago, DeepSeek v3 triggered a

How this evolves remains uncertain. Will enterprises accept 77x cost premiums indefinitely? Will Chinese models gain enterprise trust? Will GPT-5's marginal improvements justify exponential training costs? It seems inevitable that something will have to shift.

What we do know: right now, all these assets rise together. NVIDIA sells chips to everyone. OpenAI and Anthropic race toward

The IPO Window Reopens

After three years of drought, the IPO market in the US shows genuine life. Circle's June debut delivered a 168% first-day pop, trading at

But Figma's late-July IPO marked the real turning point. The design platform priced at

The queue builds. Klarna filed confidentially in June, targeting September. Discord shows 45% IPO probability in betting markets. Databricks, at

Fund Portfolio Update

Performance Metrics

While markets wrestle with AI valuations, the Fund's portfolio companies keep shipping product and signing customers.

At the end of Q2, performance metrics stand as follows: IRR at 15.65%, TVPI (Total Value to Paid-In Capital) at 1.27x, and DPI at 0.14x. The Fund portfolio averaged 61% annualised revenue growth. Four companies reached inflection points where product development translated into customer acceleration.

Portfolio Momentum

Several Fund portfolio companies demonstrated exceptional quarter-on-quarter growth:

· Popp led with 67% quarter-on-quarter revenue growth as their agentic AI for HR and recruitment found product-market fit. Enterprises discovered that AI agents handling initial candidate screening and scheduling cut hiring cycles from weeks to days.

· ThingTrax grew 23% quarter-on-quarter as F&B manufacturers accelerated adoption of their AI-powered quality control systems. When detecting contamination prevents million-dollar recalls, ROI calculations become simple.

· Duel maintained 17% quarter-on-quarter growth following their impressive

· OctaiPipe delivered 15% quarter-on-quarter growth as data centres scrambled to optimise cooling systems. Their AI reduces facility power consumption by 30%-critical when every watt saved enables more operational capability.

The Physical AI Opportunity

The Fund portfolio increasingly demonstrates how AI creates value in the physical world. OctaiPipe optimises data centre energy. ThingTrax ensures the highest standards of food-safety. Bench accelerates aerospace and automotive design cycles. FreightSuite automates logistics operations with AI. Each shows the same pattern: AI solving expensive problems with measurable ROI.

New Investments

Q2 saw the Fund finalise due diligence on three investments that subsequently closed or will close in Q3:

· Ploy solves the identity sprawl problem that kills enterprises. Most companies have employees with access to hundreds of systems they never use-95% of permissions sit idle. When an employee leaves, IT scrambles through dozens of platforms revoking access. Ploy maps every permission across every system, then automates the mess away. Their just-in-time access means employees get what they need when they need it, then lose it automatically. For companies drowning in compliance audits and access reviews, Ploy turns months of manual work into automated workflows.

· Fit Collective attacks fashion's

The Fund is also completing due diligence on a deep tech company that's building machine-agnostic autonomous systems for heavy machinery and warehouse logistics. Their technology retrofits existing industrial equipment-from forklifts to construction vehicles-with AI that enables safe, efficient autonomous operation.

Portfolio Spotlight: Bench

Bench exemplifies how agentic AI transforms traditional engineering workflows. Their platform gives aerospace and automotive engineers AI design assistants that optimise across thousands of variables-payload capacity, range, weight distribution, aerodynamics-in hours instead of months.

The key insight: engineers spend 70% of their time on iterative optimisation that AI handles better. When every kilogram saved in aerospace design means millions in lifetime fuel costs, Bench's AI pays for itself on the first project. Early customers report 10x acceleration in design cycles with superior outcomes.

Investment Thesis Evolution

As it approaches the end of the investment period, the Fund is planning just a few more investments to complete its portfolio. The Fund's focus sharpens on three areas where European companies demonstrate clear advantages:

· Agentic AI: Beyond chatbots and copilots, they see AI agents handling complex, multi-step workflows. European companies building vertical specific agents avoid competing with OpenAI and Anthropic on general intelligence.

· Physical AI: The next

· Cybersecurity: As AI capabilities expand, so do attack surfaces. Every new advance in AI creates opportunities both for perpetrators and for tech companies that can catch them.

Looking Forward

The Fund's portfolio demonstrates what patient capital achieves. While markets ignore Chinese models pricing at 1/77th and obsess over NVIDIA's next quarter, our companies quietly compound value by solving real problems for real customers. The winners won't be those with the biggest models or most hype, but those who translate AI capabilities into customer outcomes.

Markets will continue their volatility. Open-source models will keep improving. Valuations will correct. Through it all, the fundamental equation holds: companies creating genuine value compound through the cycle.

|

SuperSeed Capital Limited |

||||||||

|

Condensed Statement of Comprehensive Income |

||||||||

|

for the period 1 January 2025 to 30 June 2025 |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

1 April 2025 |

|

1 January 2025 |

|

1 January 2025 |

|

1 January 2024 |

|

|

|

to |

|

to |

|

to |

|

to |

|

|

|

30 June 2025 |

|

31 March 2025 |

|

30 June 2025 |

|

30 June 2024 |

|

|

|

£ |

|

£ |

|

£ |

|

£ |

|

|

|

|

|

|

|

|

||

|

Income |

|

|

|

|

|

|

||

|

Realised gain on investments held at fair value through profit or loss |

|

- |

|

39,285 |

|

39,285 |

|

57,200 |

|

Unrealised gain/(loss) on investments held at fair value through profit or loss |

|

23,604 |

|

(9,803) |

|

13,801 |

|

106,066 |

|

Other income |

|

92 |

|

69 |

|

161 |

|

3,456 |

|

Total income |

|

23,696 |

|

29,551 |

|

53,247 |

|

166,722 |

|

|

|

|

|

|

|

|

|

|

|

Expenses |

|

|

|

|

|

|

||

|

Administration fees |

|

7,842 |

|

7,843 |

|

15,685 |

|

15,453 |

|

Audit fees |

|

6,233 |

|

6,164 |

|

12,397 |

|

12,432 |

|

Directors' fees |

|

5,000 |

|

5,000 |

|

10,000 |

|

10,000 |

|

Insurance |

|

- |

|

1,036 |

|

1,036 |

|

1,036 |

|

Legal & professional fees |

|

10,802 |

|

9,310 |

|

20,112 |

|

23,554 |

|

Loan interest |

|

10,141 |

|

2,164 |

|

12,305 |

|

5,380 |

|

Management fees |

|

2,004 |

|

2,003 |

|

4,007 |

|

3,304 |

|

Regulatory fees |

|

3,534 |

|

5,142 |

|

8,676 |

|

9,349 |

|

Sundry expenses |

|

- |

|

93 |

|

93 |

|

547 |

|

Total expenses |

|

45,556 |

|

38,755 |

|

84,311 |

|

81,055 |

|

|

|

|

|

|

|

|

|

|

|

Total (loss) / gain and comprehensive (loss) /income for the period |

|

(21,860) |

(9,204) |

|

(31,064) |

|

85,667 |

|

|

|

|

|

|

|

|

|

||

|

Basic earnings per share |

|

(0.0092) |

|

(0.0039) |

|

(0.0131) |

|

0.0362 |

|

|

|

|

|

|

|

|

|

|

|

Diluted earnings per share |

|

(0.0092) |

|

(0.0039) |

|

(0.0131) |

|

0.0362 |

|

|

|

|

|

|

|

|

|

|

|

All the above items are derived from continuing operations. |

|

|

|

|

|

|

||

|

SuperSeed Capital Limited |

|||||

|

Condensed Statement of Financial Position |

|||||

|

as at 30 June 2025 |

|||||

|

|

|

|

|

|

|

|

|

30 June 2025 |

|

31 March 2025 |

|

31 December 2024 |

|

|

£ |

|

£ |

|

£ |

|

|

|

|

|

|

|

|

Non-current assets |

|

|

|

|

|

|

Investments |

3,277,103 |

|

3,205,943 |

|

3,050,658 |

|

Total non-current assets |

3,277,103 |

|

3,205,943 |

|

3,050,658 |

|

|

|

|

|

|

|

|

Current assets |

|

|

|

|

|

|

Trade and other receivables |

9,900 |

|

4,249 |

|

7,417 |

|

Cash and cash equivalents |

39,909 |

|

41,877 |

|

27,870 |

|

Total current assets |

49,809 |

|

46,126 |

|

35,287 |

|

|

|

|

|

|

|

|

Total assets |

3,326,912 |

|

3,252,069 |

|

3,085,945 |

|

|

|

|

|

|

|

|

Current liabilities |

|

|

|

|

|

|

Trade and other payables |

29,941 |

|

33,379 |

|

43,403 |

|

Loans payable |

360,553 |

|

260,412 |

|

75,060 |

|

Total current liabilities |

390,494 |

|

293,791 |

|

118,463 |

|

|

|

|

|

|

|

|

Total liabilities |

390,494 |

|

293,791 |

|

118,463 |

|

|

|

|

|

|

|

|

Net assets |

2,936,418 |

|

2,958,278 |

|

2,967,482 |

|

|

|

|

|

|

|

|

Equity |

|

|

|

|

|

|

Share capital |

2,369,743 |

|

2,369,743 |

|

2,369,743 |

|

Retained earnings |

566,675 |

|

588,535 |

|

597,739 |

|

Total equity |

2,936,418 |

|

2,958,278 |

|

2,967,482 |

|

|

|

|

|

|

|

|

Net asset value per ordinary share |

1.2413 |

|

1.2505 |

|

1.2544 |

|

|

|

|

|

|

|

|

Net asset value per ordinary share inclusive of notional management fee* |

1.2050 |

|

1.2142 |

|

1.2143 |

|

|

|

|

|

|

|

|

*In accordance with Section 13.1.2 of the Alternative Investment Management Agreement between the Company and SuperSeed Ventures LLP (the "Manager") dated 21 January 2022, the Manager is entitled to receive from the Company a management fee of 20% of the aggregate net realised profits on investments, provided that no fee shall be payable in connection with any investment in respect of which the Manager already receives a fee. If all assets were to be realised at the current valuation, the Manager would be due management fees in the amount of |

|||||

|

|

|

|

|

|

|

|

SuperSeed Capital Limited |

||||||

|

Condensed Statement of Changes in Equity |

||||||

|

for the period 1 January 2025 to 30 June 2025 |

||||||

|

|

|

|

|

|

|

|

|

|

|

Share Capital |

|

Retained Earnings |

|

Total |

|

|

|

£ |

|

£ |

|

£ |

|

|

|

|

|

|

|

|

|

Balance as at 1 January 2025 |

|

2,369,743 |

|

597,739 |

|

2,967,482 |

|

Total comprehensive loss for the period |

|

- |

|

(31,064) |

|

(31,064) |

|

|

|

|

|

|

|

|

|

Balance as at 30 June 2025 |

|

2,369,743 |

|

566,675 |

|

2,936,418 |

|

|

|

|

|

|

|

|

|

SuperSeed Capital Limited |

||||||

|

Condensed Statement of Cash Flows |

||||||

|

for the period 1 January 2025 to 30 June 2025 |

||||||

|

|

|

|

|

|

|

|

|

|

|

1 April 2025 |

|

1 January 2025 |

|

1 January 2024 |

|

|

|

to |

|

to |

|

to |

|

|

|

30 June 2025 |

|

30 June 2025 |

|

30 June 2024 |

|

|

|

£ |

|

£ |

|

£ |

|

Cash flows used in operating activities |

|

|

|

|

|

|

|

Net cash flow used in operating activities |

|

(44,412) |

|

(87,790) |

|

(82,438) |

|

|

|

|

|

|

|

|

|

Cash flows (used in)/from investing activities |

|

|

|

|

|

|

|

Net cash flow (used in)/from investing activities |

|

(47,556) |

|

(173,359) |

|

26,396 |

|

|

|

|

|

|

|

|

|

Cash flows from / (used in) financing activities |

|

|

|

|

|

|

|

Net cash flow from / (used in) financing activities |

|

90,000 |

|

273,188 |

|

(5,381) |

|

|

|

|

|

|

|

|

|

Net movement in cash and cash equivalents during the period |

(1,968) |

|

12,039 |

|

(61,423) |

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents at the beginning of the period |

41,877 |

|

27,870 |

|

99,185 |

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents at the end of the period |

39,909 |

|

39,909 |

|

37,762 |

|

|

|

|

|

|

|

|

|

|

SuperSeed Capital Limited |

||||||

|

Investment Analysis |

||||||

|

for the period 1 January 2025 to 30 June 2025 |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

30 June 2025 |

|

31 December 2024 |

|

|

|

|

|

£ |

|

£ |

|

|

|

|

|

|

|

|

|

Cost |

|

|

2,382,843 |

|

2,170,199 |

|

|

Cumulative movement in value |

|

|

894,260 |

|

880,459 |

|

|

Fair value |

|

|

3,277,103 |

|

3,050,658 |

|

|

|

|

|

|

|

|

|

|

Investment fair value can be further analysed as follows: |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

1 April 2025 |

|

1 January 2025 |

|

1 January 2024 |

|

|

|

to |

|

to |

|

to |

|

|

|

30 June 2025 |

|

30 June 2025 |

|

31 December 2024 |

|

|

|

£ |

|

£ |

|

£ |

|

Cost |

|

|

|

|

|

|

|

Cost at beginning of the period |

2,335,287 |

|

2,170,199 |

|

1,875,058 |

|

|

Cost of investment - settled |

47,556 |

|

379,775 |

|

905,788 |

|

|

Cost of investment - sold |

- |

|

(167,131) |

|

(610,647) |

|

|

Total cost of investment |

2,382,843 |

|

2,382,843 |

|

2,170,199 |

|

|

|

|

|

|

|

|

|

|

Fair value movement |

|

|

|

|

|

|

|

Fair value adjustment at beginning of the period |

870,656 |

|

880,459 |

|

557,954 |

|

|

Revaluation of underlying investments |

23,604 |

|

13,801 |

|

322,505 |

|

|

|

|

894,260 |

|

894,260 |

|

880,459 |

|

Fair value of investments |

3,277,103 |

|

3,277,103 |

|

3,050,658 |

|

|

|

|

|

||||

RNS may use your IP address to confirm compliance with the terms and conditions, to analyse how you engage with the information contained in this communication, and to share such analysis on an anonymised basis with others as part of our commercial services. For further information about how RNS and the London Stock Exchange use the personal data you provide us, please see our Privacy Policy.